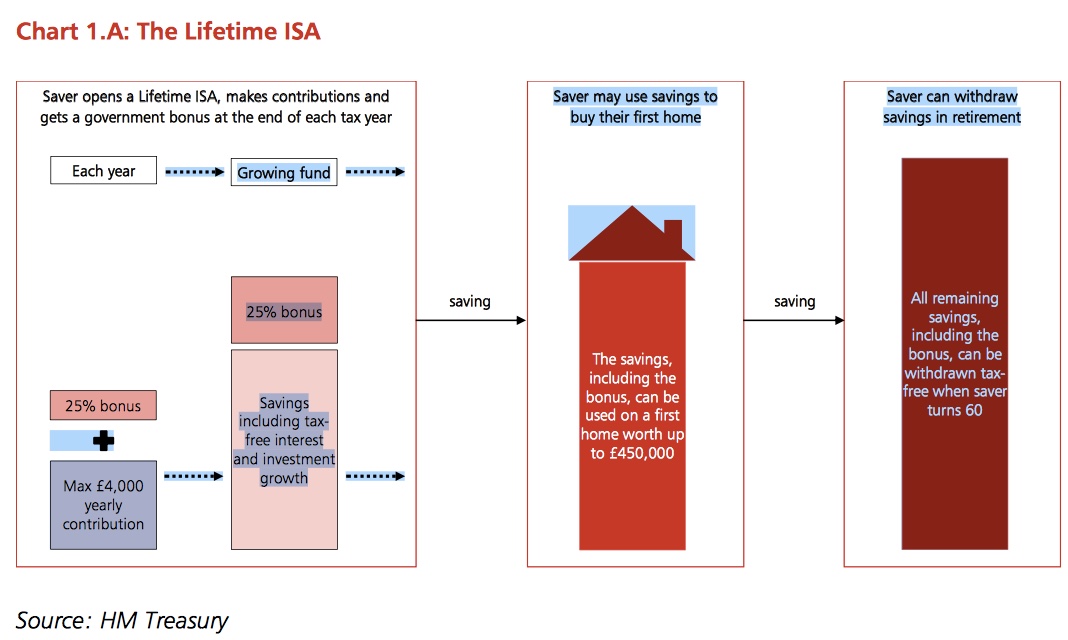

Introduction to the Lifetime ISA

The Lifetime Individual Savings Account (ISA) has become an essential savings tool for many individuals in the UK, especially for first-time homebuyers and those planning for retirement. Launched in 2017, the Lifetime ISA allows individuals to save up to £4,000 each year, with the government offering a generous 25% bonus on contributions. As the cost of living continues to rise and buying a home becomes increasingly challenging, understanding the nuances of the Lifetime ISA is critical for effective financial planning.

Key Features of the Lifetime ISA

The Structure of the Lifetime ISA is designed with specific benefits:

- Government Bonus: For every £4,000 saved in a tax year, the government contributes a bonus of £1,000, up to a maximum of £32,000 by age 50.

- Tax Benefits: Like other types of ISAs, any interest or investment gains made within a Lifetime ISA are free of tax.

- Withdrawal Options: Funds can be withdrawn for a first home purchase costing up to £450,000, or for retirement after age 60 without facing penalties. However, withdrawals for any other purpose will incur a 25% charge on the amount withdrawn.

Recent Developments and Current Trends

Recent reports suggest an increase in interest in Lifetime ISAs, largely due to rising house prices and the difficulties faced by young adults in entering the property market. According to a study conducted by the Housing, Communities & Local Government Committee, the proportion of first-time buyers reached its highest level in 2022, partly attributed to the benefits of the Lifetime ISA. In the present economic landscape, individuals are becoming more aware of saving strategies that can help them achieve homeownership sooner.

Potential Challenges and Considerations

While the Lifetime ISA offers many benefits, potential savers should be aware of some caveats:

- Restricted Withdrawals: Many users may find the restrictions on withdrawals and associated penalties problematic if they wish to use the funds for purposes other than housing or retirement.

- Contribution Limits: The £4,000 annual limit may not be sufficient for some savers who are looking to build capital quickly.

Conclusion

The Lifetime ISA presents a valuable opportunity for young savers looking to purchase their first home or build their retirement savings. With the government bonus providing a crucial boost, it has emerged as a noteworthy option in the financial toolkit of UK citizens. However, potential savers must critically assess their financial plans, considering the set limits and withdrawal penalties. With continued education and awareness, the Lifetime ISA can play a significant role in fostering financial security for future generations.