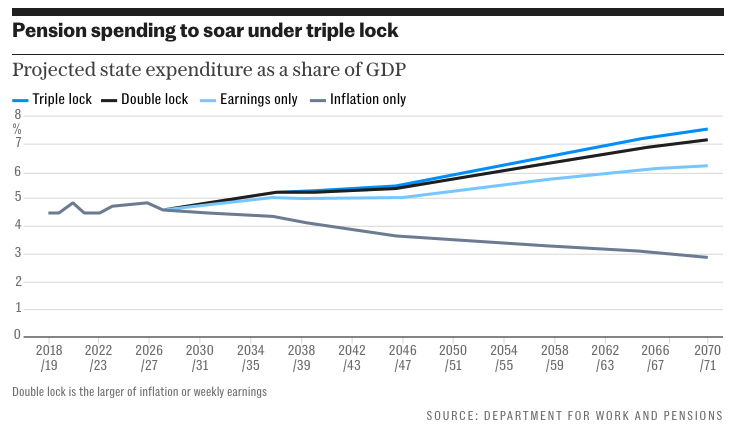

Introduction to the Triple Lock State Pension

The triple lock mechanism is crucial for the financial security of retirees in the United Kingdom. Introduced in 2010, it guarantees that the state pension will increase each year by whichever is highest among inflation, 2.5%, or average earnings growth. As the cost of living continues to rise, particularly following the pandemic and recent economic challenges, the announcement of the state pension increase for the upcoming year carries significant weight for millions of pensioners.

Recent Developments and Increases for 2023

In September 2023, the government confirmed that state pension payments would increase by 8.5% from April 2024, based on the latest inflation figures. This rise will see the full new state pension rise from £203.85 to approximately £221.00 per week, providing a welcome boost for retirees facing soaring living costs. The inflation rate, which has been influenced by rising energy prices and other factors, has played a pivotal role in this increase.

Impact on Pensioners

This substantial increase under the triple lock is expected to greatly benefit approximately 12.5 million retirees across the UK. The additional funds will assist many in managing their day-to-day expenses, particularly in light of rising prices in essential goods such as food and energy. Moreover, this increase is vital for ensuring that pensioners can maintain a decent standard of living, as many rely solely on their state pension for income.

Political Implications

The triple lock policy has not been without controversy, especially amid discussions on public spending and the sustainability of pension schemes. Some political factions have proposed reforming or temporarily suspending the triple lock in favour of a more fiscally responsible approach. However, the current government has reaffirmed its commitment to maintaining the triple lock, underlining its importance to voters, particularly older constituents.

Conclusion and Future Projections

The projected increase in the state pension, fuelled by the triple lock, underscores the significance of this mechanism in safeguarding the financial wellbeing of retirees. As inflation and living costs remain volatile, the continuation of such policies will be critical in the coming years. Stakeholders advocate for preserving the triple lock amidst ongoing debates about its long-term viability, as financial stability for retirees remains a fundamental concern in UK socio-economic discussions. Looking ahead, the government will need to navigate these challenges carefully to ensure the accessibility and sustainability of the state pension system for future generations.